How accurate are the official reports? The IMF's WEO and the BIS Annual Report, under review

A didactic study · starts plain, ends as a report: history, documented biases and track record of the two most-read economic documents in the world

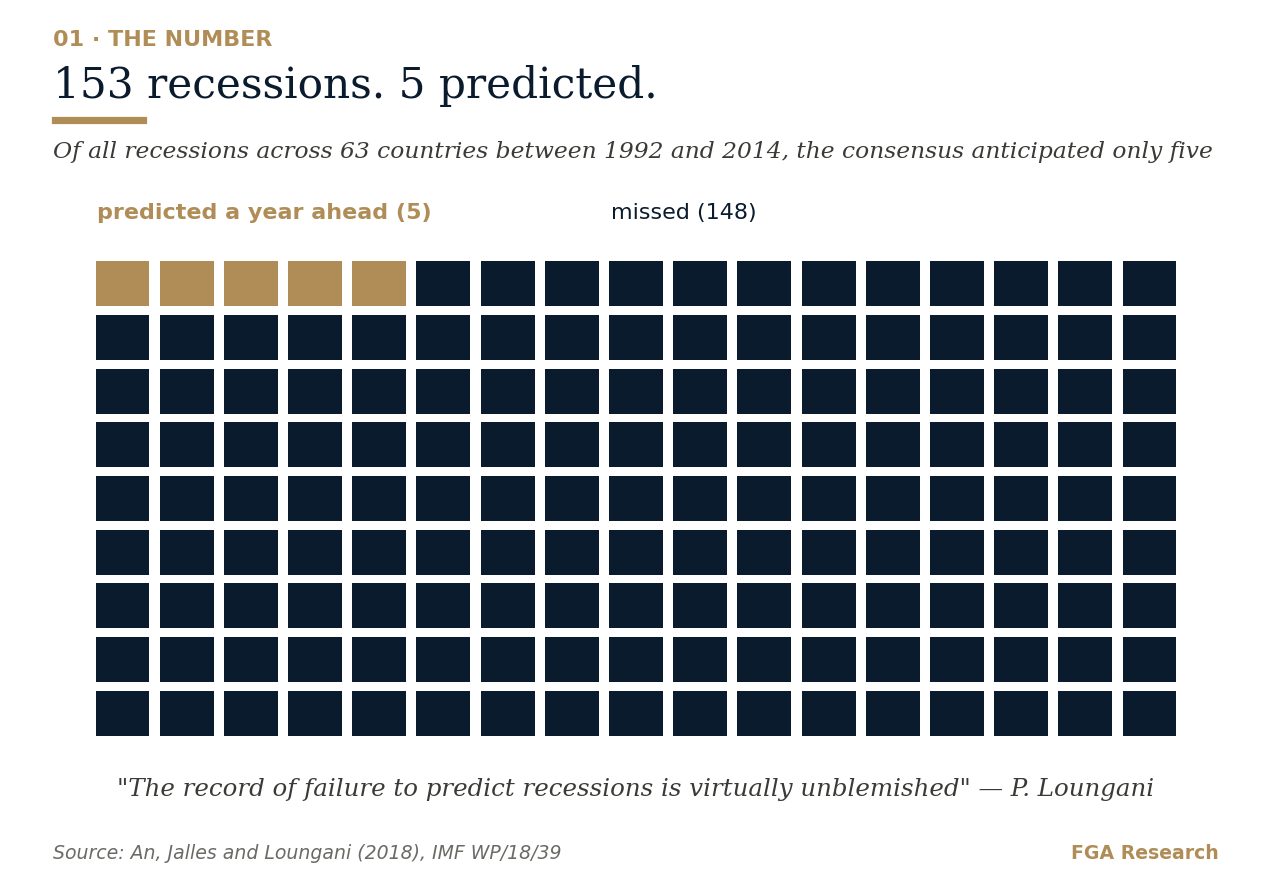

The verdict. The IMF's WEO forecasts levels, and its record at turning points has been measured: of 153 recessions between 1992 and 2014, the consensus anticipated only 5. The BIS report monitors vulnerabilities, and its record too: it warned of 2008 from 2003 — and called for rate hikes in 2011, three years too early. Neither is an oracle. We use them for what they are: two first-class inputs, with known strengths and weaknesses — read through a methodology of our own.

First, in plain words

If this is not your trade, one image is enough.

The IMF produces the weather forecast of the world economy. Twice a year — plus two updates — it publishes how much each country will grow, the way the weatherman says whether it rains tomorrow. That forecast is called the World Economic Outlook, the WEO.

The BIS is something else: it is the building inspector. It does not tell you whether it rains tomorrow. It checks the beams: how much debt has accumulated, who holds it, and where the crack is showing. Its annual diagnosis has come out every June for nearly a century.

Why should any of this matter to a normal person? Because these two documents move decisions that end up in your life: the interest rates that price your mortgage, government budgets, the portfolios where your pension sits. When a headline says "the IMF projects" or "the BIS warns", it is quoting one of these two reports — almost always without telling you the essential part: how often they actually get it right. And misreading them is not free: it is paid in decisions.

Keep one number in mind as you read: of 153 recessions, the experts anticipated 5. By the end of this piece you will understand why that figure does not make the experts useless — it makes it useless to ask them for what they cannot give.

The piece starts gentle and hardens as it goes: by the end it is a report. Stay as long as you like — the 30-second summary waits below.

Of 153 recessions across 63 countries (1992-2014), the consensus anticipated only 5 a year ahead. FGA illustration after An, Jalles and Loungani (2018).

What they are, and where they come from

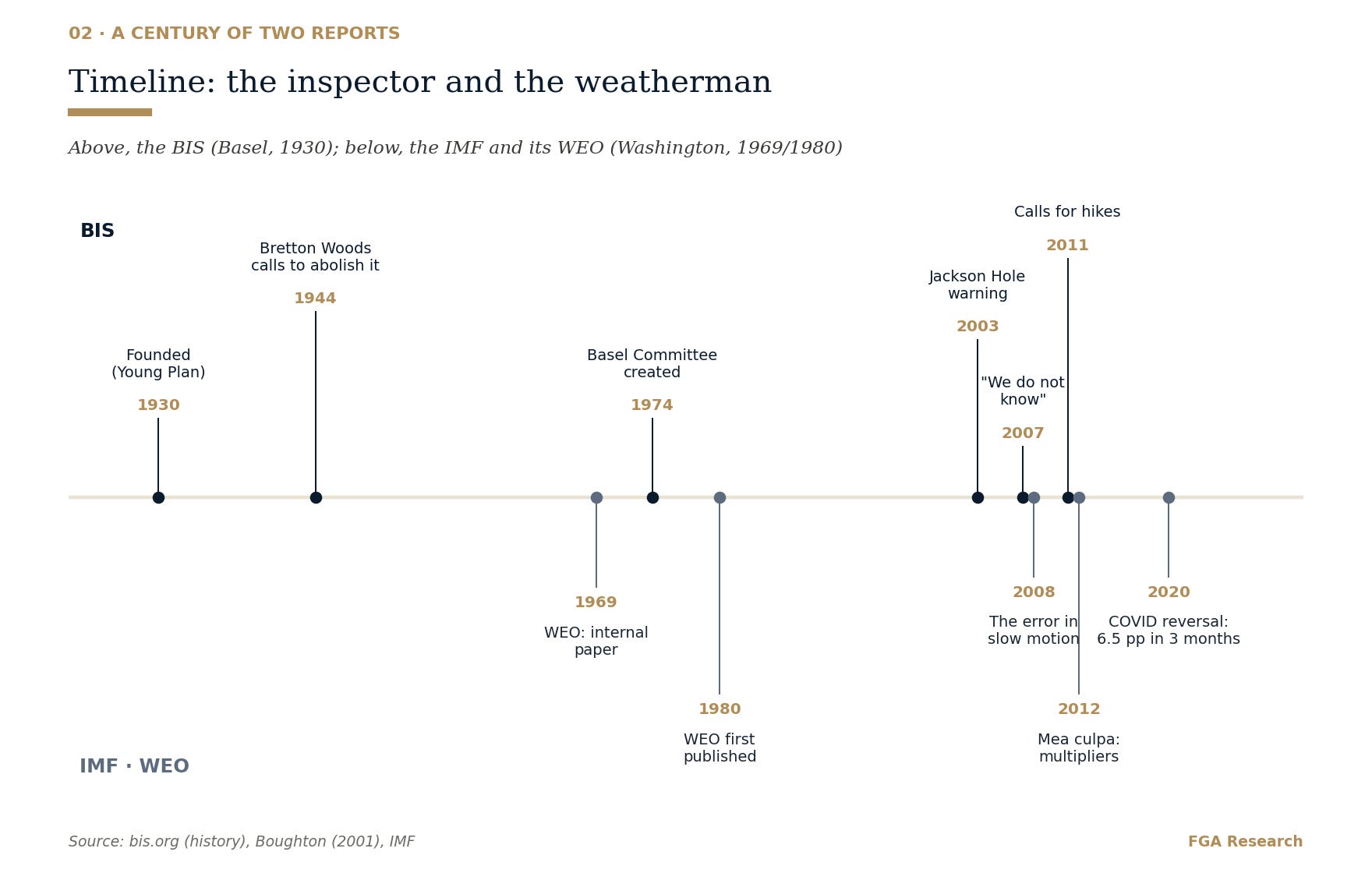

The World Economic Outlook was born as an internal staff paper at the IMF in June 1969, for an informal Board discussion. For eleven years it circulated only internally. In May 1980 it was published for the first time; in 1984 public interest made it semiannual (April and October), and crises added special editions — December 1997 (Asia), December 2001 (after 9/11) — until the January and July updates became standard. Today its database covers 196 economies, projects five years out, and is public and free: probably the largest statistical public good in the economic world.¹

The BIS Annual Report is older than the IMF itself. The Bank for International Settlements was founded on 20 January 1930 under the Young Plan to administer Germany's Versailles reparations — hence "Settlements". It opened in Basel on 17 May 1930 and is the world's oldest international financial institution; it has published its annual report since 1931. Its biography has a dark chapter — during World War II it accepted from the Reichsbank 3.7 tonnes of gold that turned out to be looted from Belgium and the Netherlands, returned in 1948 — and a near-death: the 1944 Bretton Woods conference adopted a resolution calling for its liquidation "at the earliest possible moment". It survived. Today it groups 63 central banks representing about 95% of world GDP, and has hosted the Basel Committee since 1974 — the source of Basel I, II and III.²

Two genealogies that explain two temperaments. The IMF was born to coordinate policy among governments: its numbers are read in 190 capitals and negotiated with 190 sensitivities. The BIS answers only to central bankers: it can afford to be the uncomfortable voice.

A century of two reports: the BIS (above) and the IMF (below). FGA illustration.

How an official forecast is made

The WEO does not come out of one big model. It is built bottom-up: country-desk economists produce each national forecast; a central memo fixes global assumptions (oil, interest rates); successive aggregation rounds check consistency — for instance, that the world's current accounts sum to roughly zero. When the process converges, it is published.

Are the numbers politically massaged? The IMF's Independent Evaluation Office (IEO) investigated in 2014, and its answer has two parts. It found no evidence of political manipulation of WEO forecasts. But it did document the bias where it hurts: in countries under exceptional-access rescue programs — which concentrated more than 80% of the dollars disbursed — forecasts were systematically optimistic. When the lender and the forecaster are the same house, the number tends to help the program.³

The WEO's record, measured

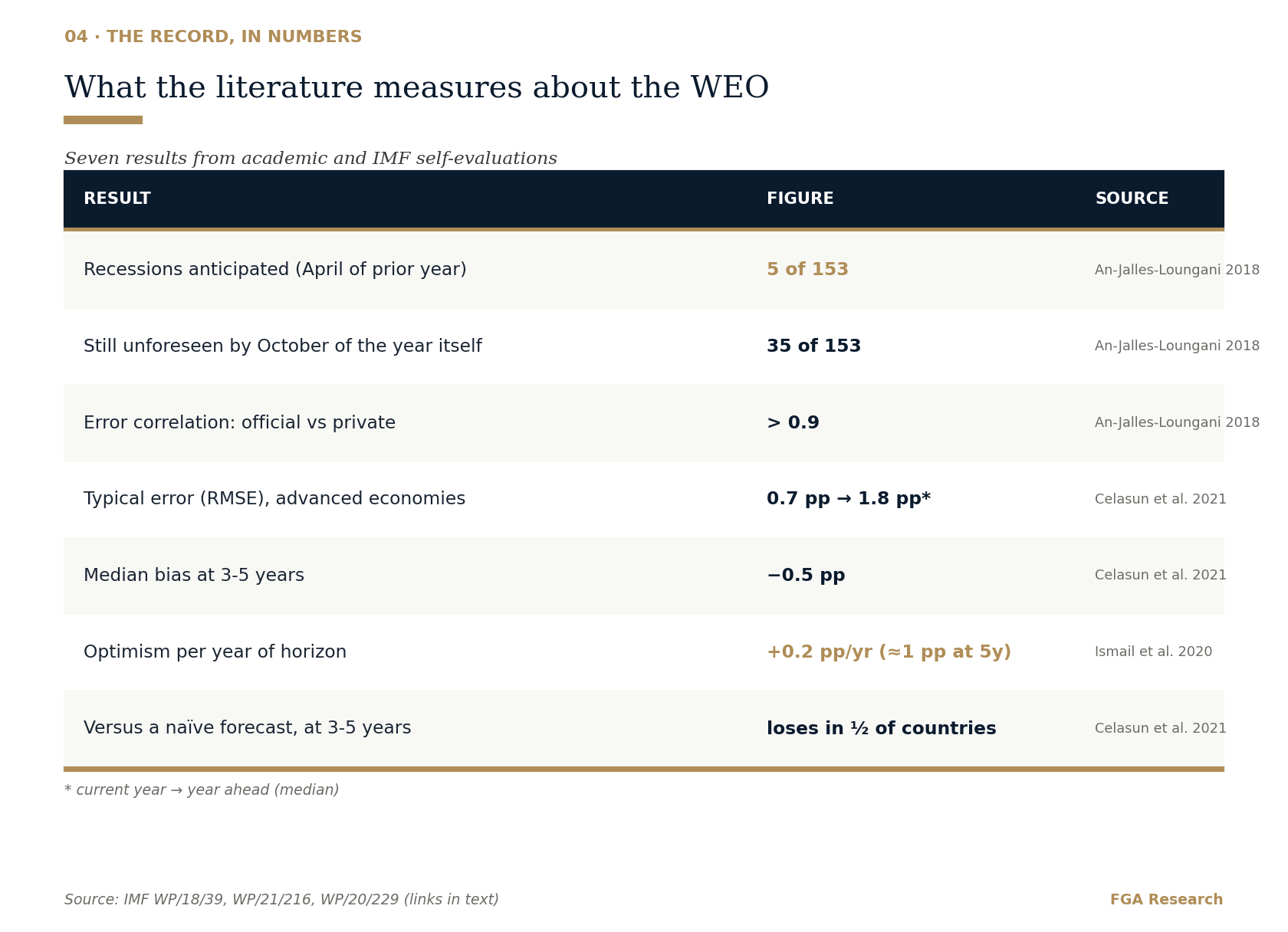

At the turning points, the result is emphatic. An IMF working paper — An, Jalles and Loungani (2018) — examined 153 recessions across 63 countries between 1992 and 2014 (1,306 country-year observations; recession occurs in 12% of them). In April of the preceding year, the consensus of forecasters expected output to fall in only 5 of the 153 cases. By October of the recession year itself — with the year nearly over — 35 were still unforeseen. And the magnitude is missed "by a wide margin until the year is almost over": on average, forecasters started from ~3% growth in advanced economies (~4.5% in emerging ones) for years that ended at −2% and −3%. Do official forecasters do worse than private ones? No: their errors are "virtually identical", with a correlation above 0.9. Prakash Loungani had already written it in 2001, examining the 1990s: "the record of failure to predict recessions is virtually unblemished."⁴

One nuance almost nobody quotes: booms are missed too. In December of a boom year, forecasts still sit ~1.5 points below actual growth. If it were only about incentives (nobody wants to announce recessions), booms would be overestimated. Missing both tails points to something deeper: limited information, and models that converge to the mean.

Two episodes tell it better than any statistic.

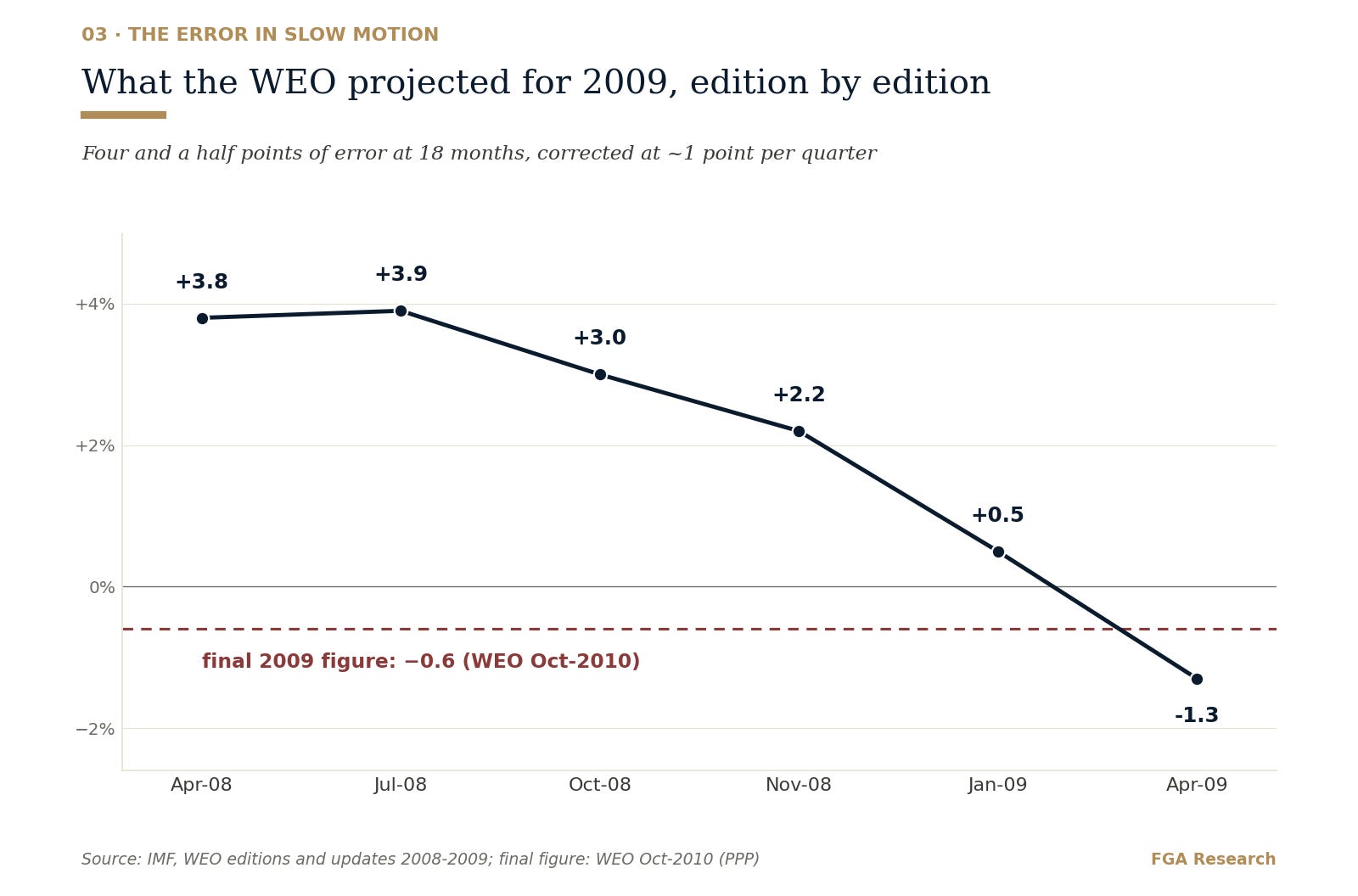

2008-09, the error in slow motion. In April 2008 — with Bear Stearns already rescued — the WEO projected 3.8% global growth for 2009. Then came the staircase down: 3.9% in July, 3.0% in October, 2.2% in November, 0.5% in January 2009, −1.3% in April. The final figure was −0.6% (and −2.0% at market exchange rates). Four and a half points of error at an eighteen-month horizon, corrected at roughly a point per quarter. It is not that nobody saw the recession: it was announced in instalments.⁵

The WEO's revision path for 2009: four and a half points of error, corrected in instalments. FGA illustration on IMF data.

2020, the fastest reversal in WEO history. In January 2020 it projected +3.3% for the year; in April, −3.0%. Six and a half points of revision in less than three months. The final figure: −3.1%. Here the forecast corrected fast — because the shock was visible to the naked eye.⁶

The bias has a known shape, and it is quantified. Timmermann (2007), in the external evaluation the IMF itself commissioned, found systematic overprediction of next-year growth (0.36-0.55 points in advanced economies) and underprediction of inflation. The 2004-2017 evaluation (Celasun et al., 2021) pinned it down by horizon and by group: the typical error (RMSE) in advanced economies runs from ~0.7 points (autumn forecast for the current year) to ~1.8 points (year ahead), and is larger in emerging and commodity economies — up to ~3.7 points at 3-5 years for fuel exporters. At short horizons the bias is small and accuracy comparable to Consensus Economics; but at 3-5 years the median error is −0.5 points, a quarter of countries accumulate optimism above one full point, and in up to half of countries the WEO loses to a naïve forecast (the historical average). And one source is identified (Ismail et al., 2020): planned fiscal adjustments. Each additional year of horizon adds ~0.2 points of optimism; over five years, a full point. The plan needs growth to cooperate, and the forecast grants it.⁷

The WEO's record according to academic and IMF self-evaluations. FGA elaboration.

Forecasters also ration their bad news. That is Nordhaus's (1987) finding, confirmed again and again in these papers: today's revisions predict tomorrow's — if a forecaster cuts, the odds are it will cut again. It is the efficiency test that the WEO and the private consensus fail alike (the stickiness only disappears inside the recession, when it is already late). In Nordhaus's words: "we break the good or bad news to ourselves slowly." The 2008-09 staircase was not bad luck: it is the pattern.⁸

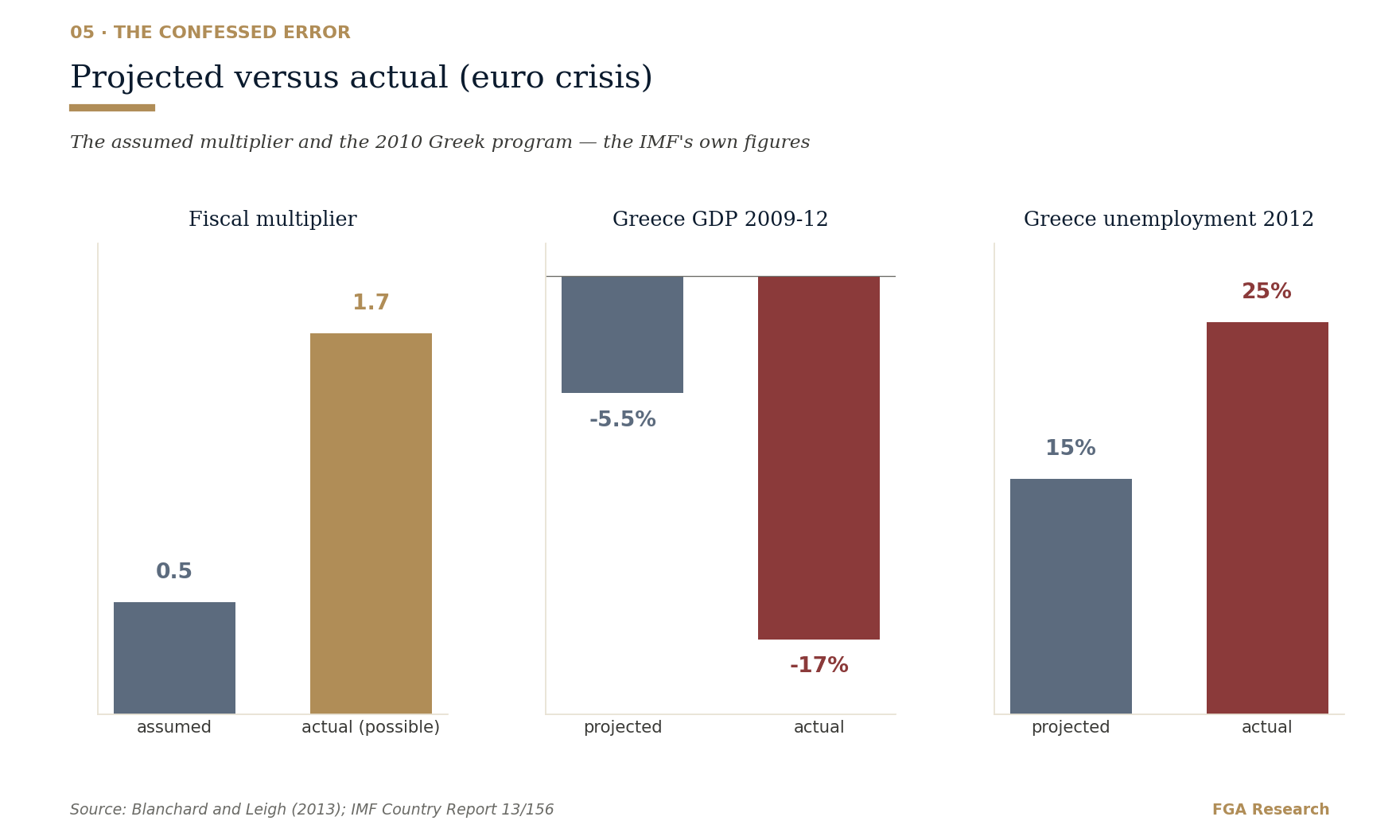

And the most expensive error is confessed in writing. In October 2012 the IMF published, in its own flagship, the box "Are We Underestimating Short-Term Fiscal Multipliers?", which Blanchard and Leigh turned into a paper in 2013. The finding: euro-crisis forecasts assumed a fiscal multiplier of ~0.5 — each euro of cuts would cost 50 cents of GDP. Actual multipliers were "substantially above 1", possibly around 1.7. Across 26 European economies, each point of planned consolidation was associated with a full point of GDP lost relative to forecast (coefficient −1.1; R² ≈ 0.5). The consequence has a name: Greece. The 2010 program projected a GDP decline of 5.5% between 2009 and 2012; the actual fall was 17%, with unemployment at 25% where 15% had been projected. The IMF's own post-mortem (2013) calls them "notable failures". The second half must be said too: it was the IMF itself that measured, published and corrected its error. Few private forecasters do that.⁹

The confessed error: assumed versus actual multiplier, and the Greek program. FGA illustration after Blanchard-Leigh (2013) and IMF (2013).

The BIS: the one that warned — and the one that always warns

The 2003 warning is documented, not legend. At the August 2003 Jackson Hole symposium, Claudio Borio and William White — the BIS's Economic Adviser from 1995 to 2008 — presented the thesis that a liberalised financial system, combined with monetary policy that only watches near-term inflation, lets financial imbalances build up unchecked. They proposed what was then unthinkable: raising rates when credit runs hot, even with inflation quiet. Greenspan, present, defended the opposite doctrine at that same symposium — let it run and clean up afterwards.¹⁰

The BIS Annual Report of June 2007 — weeks before August blew up — raises the warning to official text. Three literal quotes: "virtually no one foresaw the Great Depression of the 1930s, or the crises which affected Japan and Southeast Asia… each downturn was preceded by a period of non-inflationary growth exuberant enough to lead many commentators to suggest that a 'new era' had arrived." On securitisations: "who now holds these risks, and can they manage them adequately? The honest answer is that we do not know." And the warning that tail events "might at some point have much higher costs than is commonly supposed." When the crisis hit, Der Spiegel titled its profile of White "The Man Nobody Wanted to Hear".¹¹

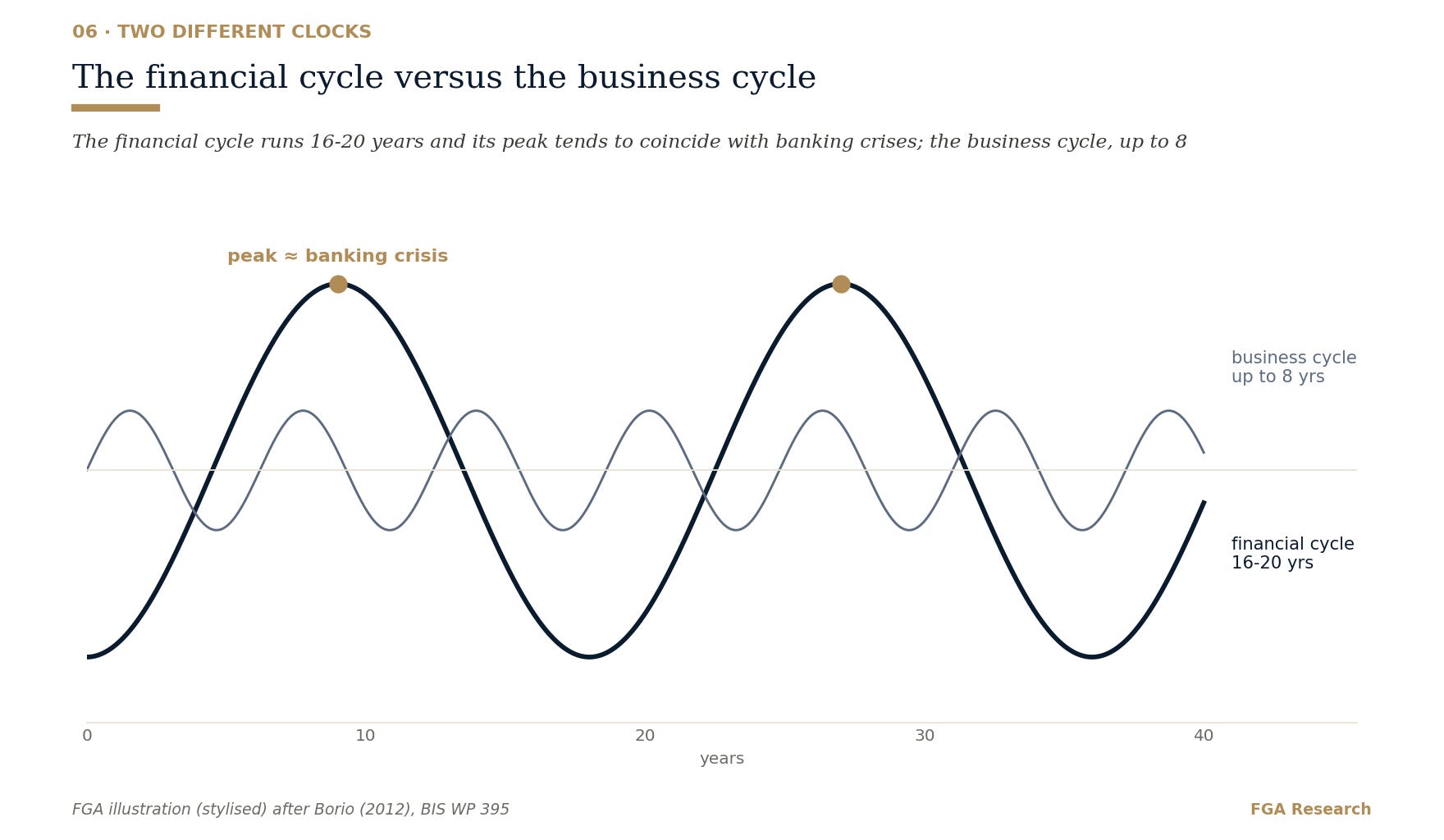

The framework behind it has numbers. Borio (2012) measured the financial cycle — the joint swing of credit and property prices — in industrialised economies: it lasts 16 years on average (nearly 20 in cycles peaking after 1998), against at most 8 for the classic business cycle. Its peaks coincide with banking crises — only three exceptions since 1985. And recessions that fall in its contraction phase are ~50% deeper.¹²

The financial cycle (16-20 years) versus the business cycle (up to 8). FGA schematic after Borio (2012).

From that literature came an operational indicator, the credit-to-GDP gap, whose early-warning power is measured: an area under the ROC curve of ~0.8 up to five years before a crisis, and the debt service ratio is even sharper near the outbreak — AUC of ~0.94 in the final quarters (Drehmann and Juselius, 2014; for calibration: a medical test like the PSA scores around 0.8). Basel III adopted it officially as the guide for the countercyclical capital buffer: gap below 2 points, zero buffer; above 10, buffer at maximum. According to the Basel Committee, that rule would have required building up capital 2-3 years in advance of every major banking crisis in its sample. The world's regulator turned the BIS thesis into law.¹³

But the flip side is documented too. In June 2011, with the recovery still fragile, the BIS Annual Report literally called for "higher policy rates" and stated that "tighter global monetary policy is needed". Advanced-economy inflation then spent years below target. Krugman demolished it in 2014 in a post titled "Stability or Sadomonetarism?": "the BIS basically just wants to raise rates, and is always looking for a reason." Martin Wolf, the same week: "bad advice from Basel's Jeremiah". The BIS defence also has literature: Schularick and Taylor (2012) showed with 140 years of data across 14 countries that "credit growth is a powerful predictor of financial crises" — ignore it at your peril. But the criticism stands: the BIS gets the crises right, not the calendars. It always warns; sometimes the world takes a decade to prove it right, and sometimes it never does.¹⁴

The statistical lesson: two loss functions

None of the above is a scandal. It is elementary statistics, and it is the part of this piece you can reuse for life. Bring back the two figures from the beginning: the weatherman and the building inspector.

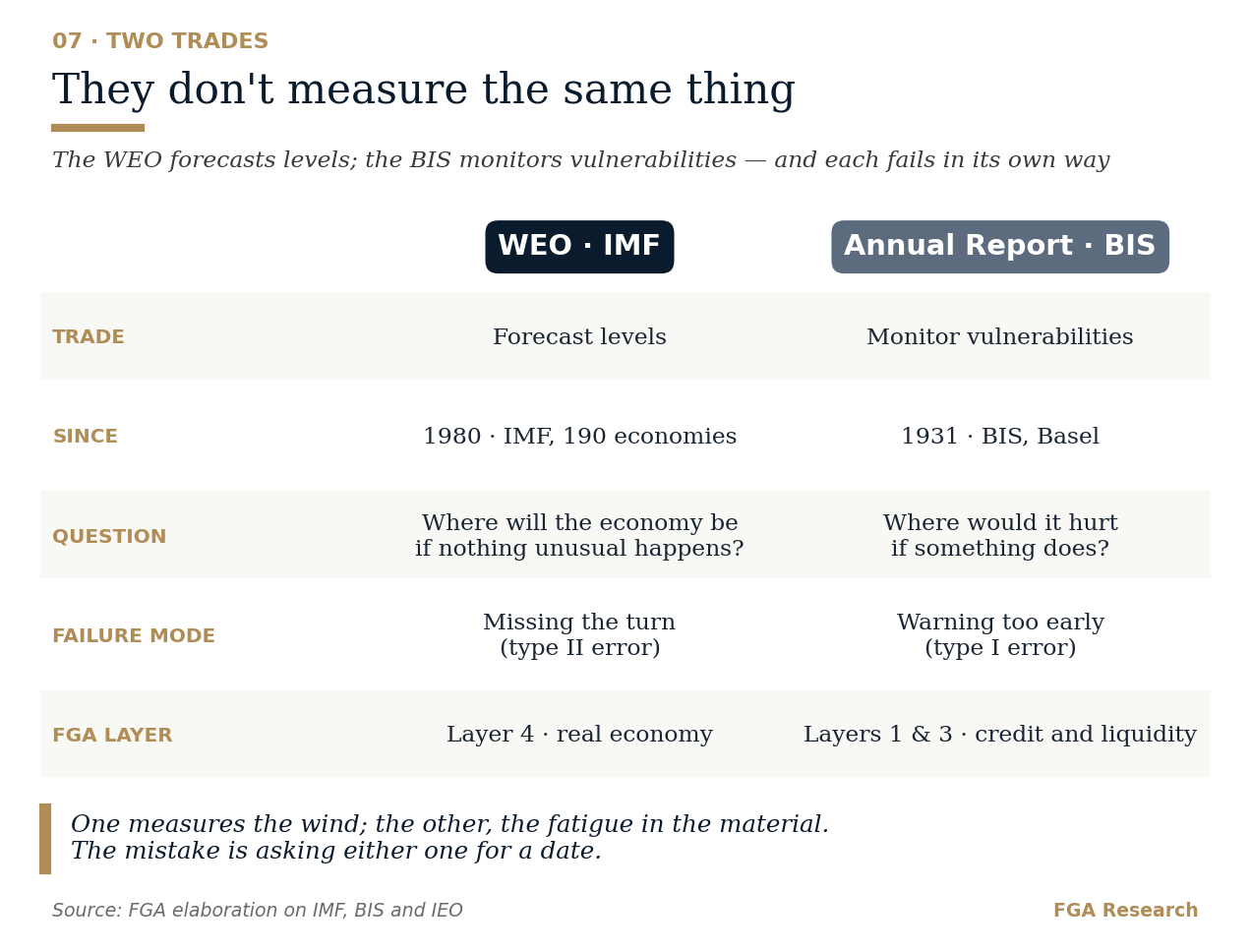

The base rate rules. In advanced economies, recessions occupy roughly 10% of quarters (122 recessions in 21 countries between 1960 and 2007; 12% of country-years in the An-Jalles-Loungani sample). A weatherman who never announces a storm is right 90% of the days. That is the trap against which everything else is measured.¹⁵

The level forecaster (WEO) minimises average error. With a 10% base rate, that pushes it mathematically toward the centre of the distribution: projecting the normal year is almost always the lowest-error bet. Its characteristic failure is type II — missing the rare event. Add the institutional incentive (the forecaster is also lender and adviser) and Nordhaus's rationing, and the 2008 staircase stops being a mystery.

The early-warning system (BIS) optimises the opposite: never missing the crisis, accepting false alarms. A serious inspector would rather close a sound building than leave a cracked one open. The classic calibration of the credit gap requires capturing at least two thirds of crises, then minimising the noise. Its characteristic failure is type I — the chronic "too early". Not a BIS defect: its mandate.

For the technical reader — two notes.Bayes and the base rate. With crises in 10% of years, an excellent indicator — one that catches 80% of crises with only 20% false alarms — is right ~3 times out of 10 when it sounds: 0.8×0.1 / (0.8×0.1 + 0.2×0.9) ≈ 0.31. Cutting false alarms to 10% lifts that to ~1 in 2. That is why no serious early-warning system promises certainty: it promises odds better than the base rate. The loss function. The literature (Alessi and Detken, 2009) formalises the regulator's choice as L = θ·(missed crises) + (1−θ)·(false alarms), where θ measures how much each type of error hurts. The WEO operates, de facto, with a low θ; the BIS, with a high one. Everything else — the optimism of one, the alarmism of the other — follows from there.¹⁶

Comparing their raw "accuracy" is therefore a category error. The right question: the WEO answers "where will the economy be if nothing unusual happens?"; the BIS answers "where would it hurt if something does?"

Two trades, two failure modes: the forecaster and the watchman. FGA elaboration.

How we put them to work — with a methodology of our own

Two things must be kept apart here, because they are often confused. Our methodology does not come from these reports. The four layers through which we read the cycle — cycle and credit, crowd, liquidity, real economy — are built on FGA's proprietary series, developed and tested over years and documented in a public working paper. The BIS and the WEO are not our method: they are two context inputs that are valuable precisely because their record — strengths and weaknesses — has been measured, as we have just seen. Once the weakness is known, you sidestep it; once the strength is known, you exploit it.

From the WEO we exploit its strength: the best map of the central scenario at short horizons and an unbeatable database. We use it as context for the real-economy layer. And we sidestep its measured weakness: we never ask it to warn us of a turn — it is proven that it will not do so in time. Watching the turn is the job of our own leading indicators, built for exactly that.

From the BIS we exploit its strength: the most serious inventory in existence of credit and liquidity fragilities. We use it as a cross-check on our cycle and liquidity layers. And we sidestep its measured weakness: it is not a calendar. A BIS warning does not by itself change the colour of any layer; our series change it, when the data confirms.

The regime — the name we give to the moment of the cycle — comes from the cross-reading of the four layers, not from any external document. That is why our verdict can agree with the BIS one month and disagree the next: the methodology is ours; they are two first-class cross-checks.

In one sentence: we don't predict, we classify — and we use the world's best forecaster and the world's best inspector knowing exactly how each one fails.

Summer 2026 is the live example. July's WEO describes a cycle that holds (3.0% global) standing on a single technological leg; June's BIS report describes exactly that leg as the vulnerability — AI capex financed with debt and circular financing (we analysed it in our reading of the BIS report). They do not contradict each other: each is doing its job. Our framework read them together in the BIS–IMF diptych — and no layer changed colour because of it.

In this series: our reading of the BIS report (30 June) · the BIS–IMF diptych (14 July, in Spanish) · this study.

In 30 seconds

The WEO (IMF, public since 1980) is the weather forecast: it projects levels for 196 economies. At short horizons, as good as the best private consensus. At the turns, it is not: 5 of 153 recessions anticipated.

The BIS report (since 1931) is the building inspector: it does not forecast, it inventories fragilities. It warned of 2008 from 2003 — and called for hikes in 2011 with inflation below target. Alarmist by design.

Opposite errors, by construction: the WEO fails type II (missing the turn); the BIS type I (over-warning). With recession only 10% of the time, both arithmetics are inevitable.

Our rule: a proprietary four-layer methodology on our own series; the WEO as central-scenario context, the BIS as a fragility cross-check — and the turn, watched with indicators built to see it. Neither one is asked for dates.

Quick user's manual

WEO: April and October (full editions), January and July (updates). Free at imf.org/weo. Reading order: chapter 1, the projections table, and the analytical chapters — where the IMF actually thinks.

BIS: Annual Report in late June; Quarterly Review in March, June, September and December. Free at bis.org. Reading order: the concluding chapter first — the house always writes it as a diagnosis.

Golden rule: always cite the document, never the press headline about the document.

Notes and sources

Boughton, J., "Keeping Score: The World Economic Outlook", official IMF history, ch. 5 · all WEO editions since 1980.

BIS, official history: foundation · World War II and Bretton Woods · member central banks · Basel Committee history · first Annual Report (1931).

IMF IEO (2014), "IMF Forecasts: Process, Quality, and Country Perspectives".

An, Z., J. Jalles and P. Loungani (2018), "How Well Do Economists Forecast Recessions?", IMF WP/18/39 · Loungani (2001), "How accurate are private sector forecasts?", International Journal of Forecasting 17(3).

IMF, WEO April 2008, ch. 1 · January 2009 update · final figure: WEO October 2010, tables.

IMF, WEO Update January 2020 · WEO April 2020 · final figure: WEO October 2021, ch. 1.

Timmermann, A. (2007), "An Evaluation of the World Economic Outlook Forecasts", IMF Staff Papers 54(1) · Celasun, Lee, Mrkaic and Timmermann (2021), IMF WP/21/216 · Ismail, Perrelli and Yang (2020), IMF WP/20/229.

Nordhaus, W. (1987), "Forecasting Efficiency: Concepts and Applications", Review of Economics and Statistics 69(4).

Blanchard, O. and D. Leigh (2013), "Growth Forecast Errors and Fiscal Multipliers", IMF WP/13/1 (also in American Economic Review 103(3)) · the original box: WEO October 2012, Box 1.1 · Greece: IMF Country Report 13/156 (2013).

Borio, C. and W. White (2004), "Whither Monetary and Financial Stability?", BIS Working Paper 147 — the paper presented at Jackson Hole, August 2003.

BIS, 77th Annual Report (June 2007), ch. VIII · White (2006), "Is price stability enough?", BIS Working Paper 205 · Der Spiegel (2009), "The Man Nobody Wanted to Hear".

Borio, C. (2012), "The financial cycle and macroeconomics: what have we learnt?", BIS Working Paper 395.

Drehmann, M. and M. Juselius (2014), "Evaluating early warning indicators of banking crises", BIS Working Paper 421 · Borio and Drehmann (2009), BIS Quarterly Review, March · Basel Committee (2010), countercyclical capital buffer guidance.

BIS, 81st Annual Report (June 2011), ch. IV · Krugman, P. (2014), "Stability or Sadomonetarism?", NYT · Wolf, M. (2014), "Bad advice from Basel's Jeremiah", Financial Times · Schularick, M. and A. Taylor (2012), "Credit Booms Gone Bust", American Economic Review 102(2).

Claessens, S. and M.A. Kose, "Recession: When Bad Times Prevail", IMF Finance & Development.

Alessi, L. and C. Detken (2009), "'Real time' early warning indicators for costly asset price boom/bust cycles", ECB Working Paper 1039.

Our own methodology: FGA Research, four-layer framework working paper, DOI 10.5281/zenodo.20709770.

Editorial and educational content, not investment advice. No buy/sell signals, no price targets.

Independence. Capital. Conviction. · FGA Research & Advisory · Est. 2006 · 33 años de estudio